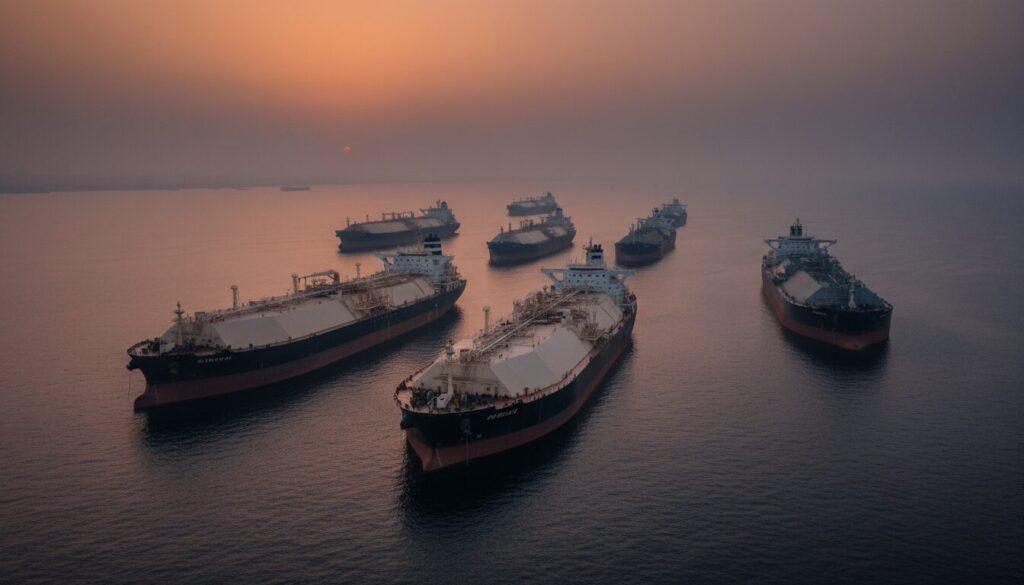

The “artery of the world” has suffered a cardiac arrest. Following the dramatic escalation of the Iran-Israel conflict on February 28, the Strait of Hormuz—the critical chokepoint through which 20% of the world’s oil and LNG flows—has reached a state of “de facto closure.”

While Tehran officially denies a full blockade, the reality on the water tells a different story. Targeted drone swarms and missile threats have rendered the passage uninsurable. Commercial traffic has collapsed from a bustling 138 ships per day to a ghostly average of just two.

For innovation leaders and supply chain strategists, this is not merely a geopolitical headline; it is a structural breakage in global trade logistics. With the Red Sea already compromised, the world now faces a “Double Blockade,” forcing a complete redrawing of maritime maps.

This article analyzes the current crisis, explores how global markets are reacting, and presents a case study on how agile logistics players are navigating this zero-traffic reality.

Why It Matters: The “Double Blockade” Reality

The Strait of Hormuz is unique. Unlike the Suez Canal, there is no viable pipeline alternative large enough to bypass it for the sheer volume of energy exports involved. The “de facto closure” has created a cascading failure across multiple industries.

Key metrics defining the crisis include:

- Energy Freeze: 20 million barrels of oil per day are effectively trapped.

- Insurance Collapse: P&I Clubs have canceled coverage for the region, citing “unquantifiable risk.” Even the US government’s announcement of a $20 billion Development Finance Corporation (DFC) reinsurance program has failed to coax shipowners back into the strait without physical naval escorts.

- Cost Explosion: War Risk Surcharges (WRS) have hit unprecedented levels. Major carriers like Hapag-Lloyd are charging upwards of $1,500 per 20ft container and $3,500 for reefers.

- Logistics Paralysis: The closure forces a reroute around the Cape of Good Hope for traffic that would normally transit Suez via the Red Sea, but for energy exports originating inside the Gulf (Saudi Arabia, UAE, Qatar, Kuwait), there is simply no exit.

As discussed in our previous analysis, Oil Tankers Avoiding Hormuz: Global Supply Chain Strategy, the inability to export from within the Gulf is fundamentally different from being unable to transit through a region. This is a blockade of origin, not just transit.

Global Trend: The Ripple Effect Across Markets

The impact of the “Hormuz Commercial Zero” phenomenon is unevenly distributed but globally felt.

1. Europe: The LNG Shock

Europe is bearing the brunt of the energy dislocation. With Qatar declaring Force Majeure on LNG production due to the inability to export, European gas futures have surged by nearly 50%. This mirrors the 2022 energy crisis but with fewer alternatives, as US LNG shipments (via the Atlantic) face their own logistical bottlenecks.

2. USA: Inflationary Pressure

While less dependent on Middle Eastern oil physically, the US markets are globally interconnected. Brent crude pushing toward $100/barrel threatens to reignite inflation. The Biden administration’s $20B reinsurance attempt highlights the severity, but as industry experts note, “Capital cannot stop a missile.”

3. Asia: The Rerouting Challenge

Asian manufacturing giants (China, Japan, South Korea) rely heavily on Middle Eastern energy. The blockade is forcing these nations to aggressively bid for Russian and South American crude, altering global trade flows and increasing the “ton-mile” demand for the few remaining tankers operating outside the Gulf.

The “Double Blockade” Impact Matrix

The following table illustrates the operational shifts caused by the simultaneous disruption of the Red Sea and the Strait of Hormuz.

| Metric | Pre-Crisis (Normal) | Current Status (Double Blockade) | Impact on Strategy |

|---|---|---|---|

| Route | Suez Canal / Hormuz Transit | Cape of Good Hope (Transit) / Blocked (Origin) | +14 Days Transit / Inventory buffers required |

| Fuel Cost | Standard | High (Longer distance) + Shortage risks | See: Rising Diesel & Iran Conflict |

| Insurance | ~0.02% of hull value | Unobtainable or >1.0% | Force Majeure declarations common |

| Logistics | Just-in-Time (JIT) | Just-in-Case (JIC) | Warehousing demand spikes in safe zones |

Case Study: Salalah as the New “Safe Harbor” and Hybrid Logistics

With ports inside the Persian Gulf (Jebel Ali, Dammam, Hamad) effectively cut off from international container line haul services, logistics providers have been forced to innovate. The standout success story in this crisis is the pivot to Salalah (Oman) and the rise of Sea-Air hybrid solutions.

The Challenge

Major carriers, including Maersk and CMA CGM, halted calls to ports inside the Strait. For a global electronics manufacturer (let’s call them “Company X”) sourcing components from Asia and assembly in Europe, this meant their regional distribution hub in Dubai was suddenly inaccessible for inbound ocean freight.

The Solution: The “Oman Bypass”

Instead of forcing ships through the dangerous Strait, logistics strategists shifted the center of gravity to the Port of Salalah, located on the Indian Ocean coast of Oman, outside the Strait of Hormuz.

- Hub Relocation: Carriers began terminating “Mother Vessel” loops at Salalah rather than Jebel Ali.

- Feeder/Land Bridge:

- Overland: Goods destined for the interior of the Arabian Peninsula are trucked overland from Oman, bypassing the maritime chokepoint (though this route has capacity limits).

- Sea-Air Swap: For high-value goods destined for Europe, Company X utilized Salalah as a transshipment point. Cargo is discharged, trucked to Salalah International Airport or Muscat, and flown to Europe.

The Innovators: Maersk and Kuehne+Nagel

Maersk rapidly adapted its “ME2” service. By utilizing the Salalah and Fujairah terminals (both outside the strait), they created a “safe zone” loop.

- Action: Maersk implemented a “Sea-Air” product offering a 50% cost saving over pure air freight and a 40% time saving over the diverted Cape of Good Hope ocean route.

- Result: While capacity is lower, high-priority cargo (pharma, automotive chips) continues to flow.

Furthermore, Hapag-Lloyd demonstrated resilience by utilizing its “Gemini Cooperation” hubs to reroute traffic smoothly around Africa, despite the cost. Their transparency regarding the surcharges allowed clients to budget effectively, contrasting with competitors who delayed communication.

This strategic shift mirrors the resilience strategies discussed in Iran Conflict: Ocean & Air Resilience Case Study, proving that geographic diversification of hubs is the only defense against chokepoint failure.

Key Takeaways for Logistics Leaders

The “Hormuz Commercial Zero” event is a wake-up call that geopolitical risks can instantly render standard routes obsolete.

1. Geographic Decoupling of Hubs

Do not rely on a single mega-hub located behind a potential chokepoint. The reliance on Jebel Ali (inside the Strait) has proven catastrophic for many. Diversify warehousing to “Open Ocean” ports (e.g., Salalah, Colombo, Singapore).

2. The Limits of Insurance

As seen with the US $20B reinsurance program, financial instruments cannot fix physical security risks. Supply chain managers must plan for physical denial of access, not just price increases. For a deeper dive on carrier reactions, see Hormuz Blockade: Japan Carrier Avoidance & Global Resilience.

3. Contractual Force Majeure Preparedness

With Qatar Energy declaring Force Majeure, buyers without robust legal frameworks in their supply contracts are left vulnerable. Review supplier contracts for “Act of War” clauses and alternative sourcing obligations.

4. Acceptance of the “Cape Premium”

The diversion around the Cape of Good Hope is no longer a temporary fix; it is a medium-term structural reality. Budgets for 2026/27 must account for the 50-100% increase in logistics costs mentioned in recent data.

Future Outlook: The Long Way Home

The “de facto closure” of the Strait of Hormuz is unlikely to resolve quickly. Even if the immediate kinetic conflict de-escalates, the risk premium has been permanently reset.

We anticipate three major shifts in the coming year:

- Permanent Rerouting: Carriers will formalize “Cape-Only” services, removing the Suez/Red Sea/Hormuz reliance from their core Asia-Europe loops. See also: CMA CGM Reverses Red Sea Return.

- Energy Supply Chain Re-alignment: Europe and Asia will accelerate the decoupling from Middle Eastern energy, boosting investment in renewables and North American LNG infrastructure to shorten supply chains.

- Revival of the “Middle Corridor”: The rail route connecting China to Europe via Central Asia and the Caspian Sea (bypassing Russia and the Middle East) will see explosive investment as the only remaining “safe” shortcut.

For the global logistics executive, the message is clear: The era of cheap, straight-line shipping is paused. Resilience now requires navigating the long way home.